Amazon.com (AMZN)

Q4 Results

We have written two notes on Amazon.com (AMZN). The first was an “Initiating Coverage” type note on 12 May 2023 and can be found here. The second was written after the Q2 2023 results and it can be found here.

This present note is after the release of the Q4 results last week.

Summary

The press reports of the numbers were along the following lines.

“Amazon (AMZN) reported its Q4 earnings beating Street estimates with $170bn in revenue versus an expected $166 bn. For the next quarter, the company forecast sales will be between $138 billion and $143.5 billion compared with Wall Street expectations of $141 billion.”

In summary, the numbers were good. AMZN beat expectations and has boosted margins greatly, in both the profitable North America business and the loss- making international business.

AMZN made huge investments in capacity, after being stretched and found wanting by the huge spike in demand in the Covid pandemic. This came to an end in 2023 and capital expenditure levels fell (a little) and Free Cash Flow improved consequently.

The retail business is increasingly dominated by third party (3P) sales where the seller is an outside merchant on “Amazon Marketplace” and Amazon provides sales, logistics and infrastructure support and services.

Significant new efficiencies have been made in delivery and logistics and these can make a huge difference given the huge scale of Amazon’s logistics operations.

The AWS Cloud business bounced back with higher revenues and margins. There is greater willingness and urgency among clients to move workloads onto the Cloud.

The earnings conference call, like those of Microsoft, Alphabet and Meta Platforms, all focused on Generative AI. The focus for all these companies has been on investments being made and experiments being done to meet potential future customer demand for Gen AI products and services.

Results summary

Revenues

Amazon beat revenue estimates by 2.2% & beat guidance by 4.0%.

It met revenue estimates for the AWS Cloud hosting business.

Amazon beat the Advertising business segment revenue estimates by 3.2%.

North American (UCAN) and international revenues were also both ahead of expectations.

Earnings

AMZN beat EBIT estimates by 26% and beat its EBIT guidance by 46%.

For AWS, AMZN beat EBIT estimate by 7.8%.

AMZN beat operating cash flow (OCF) estimates by 0.7%.

AMZN beat $0.80 GAAP EPS estimate by $0.20.

Source: The Stockmarket Nerd

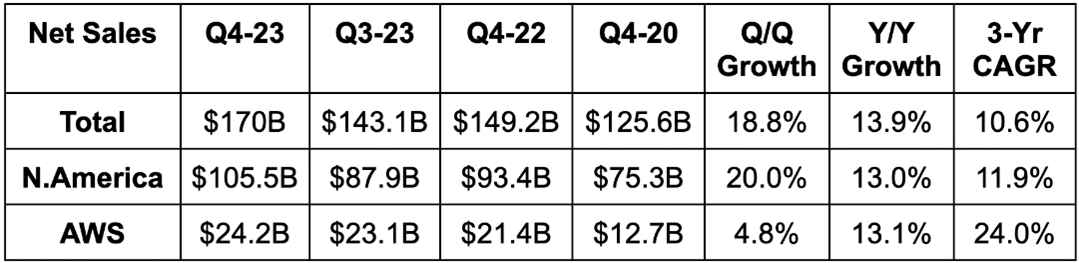

Total quarterly revenues hit a record $ 170bn of which North America was $ 106bn. AWS cloud business revenues were at $ 24bn with a growth of 13%. Microsoft Azure and Alphabet’s Google Cloud Platform (GCP)

AMZN recorded much faster revenue growth of ~30% and 26% respectively. However, AWS remains (just) the largest Cloud player and is now on an annual revenue run rate of US$ 100bn.

Margins

Source: The Stockmarket Nerd

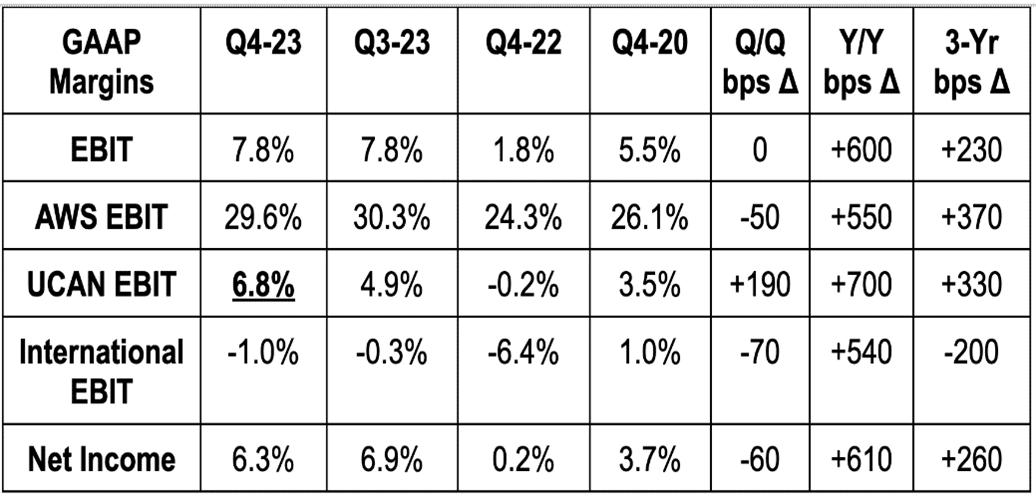

The notable feature is the impressive “across-the-board”, y-o-y margin increases of between 550 bp and 700 bp.

EBIT margin is 7.8% compared with 1.8% a year earlier.

Net Income margin is 6.3% compared with 0.2% a year earlier.

This recovery in margins reflects two things.

There is a cyclical recovery and Q$ 2022 margins were at a cyclical low. It also reflects efficiency gains and change in business composition as higher margin businesses such as AWS and Advertising have grown much faster than the core 1P retail business. This is clearly shown in the Table below:

Source: MBI Deep dives

1P retail sales (where AMZN itself is the seller) accounted for ~$76bn out of the total $169bn revenue in $Q 2023. This is just 45%. of total revenues.

The balance $94 bn comes from higher margin business such as third-party sales, AWS, Advertising and subscription services.

These businesses (AMZN revenue ex 1P) are growing much faster (18.3%) compared with the core 1P business (8.9%)

We expect this differential growth to continue and therefore, the change in business composition, will tend to increase margins and profitability over time.

There is a difference in Margins between North America (UCAN) and international. The former business is further along its evolution while some of the international businesses are at a more nascent stage. This differential margin can be seen in the chart below:

North America operating margin bottomed at -2.3% 1Q’22 and has risen to 6.1% in 4Q’23, close to the pre-pandemic high of 6.4% in 1Q’19.

International margins bottomed at -8.9% in 3Q’22 but have improved greatly since then to reach -1.0% in 4Q’23.

We will now discuss the following items which are important to understand where the company is now.

Fulfilment overhaul and margin expansion work

AWS

Generative AI

Advertising

Fulfilment overhaul and margin expansion work

Whenever we order anything from Amazon, we are always amazed (!) at the speed at which they deliver. The company has industry leading delivery times and instead of resting on their laurels, they are working to try and improve them while reducing costs.

Amazon responded to the pandemic boost in sales by a huge increase in fulfilment capacity (Capex was US$ 60bn in December 2021 and 2022- see chart below) and a last mile network, estimated to be double the size of UPS Inc, was created in 2021/2022.

The chart shows capital expenditures by Amazon. The bars are shown as negative as investment is a cash outflow. This shows that the Capital expenditure, which was $ 19bn in 2019, rose to over $ 60bn (!) in 20121 and 2022 and fell back (a little) to $ 53bn in 2023.

These are very large numbers. The company added significantly to their logistics network and, at the same time, re-engineered the network to reduce costs.

“In 2023, Amazon delivered to Prime members at the fastest speeds ever, with more than 7 billion items arriving same or next day, including more than 4 billion in the U.S. and more than 2 billion in Europe. In the U.S., this result is the combination of two things. One is the benefit of regionalization where we rearchitected the network to store items closer to customers. The other is the expansion of same-day facilities where in the U.S. in the fourth quarter, we increased the number of items delivered the same day or overnight by more than 65% year-over-year.”

“…In 2023, for the first time since 2018, we reduced our cost to serve on a per unit basis globally. In the U.S. alone, cost to serve was down by more than $0.45 per unit compared to the prior year. Lowering cost to serve allows us not only to invest in speed improvements but also afford adding more selection at lower average selling prices, or ASPs, and profitably. We have a saying that it's not hard to lower prices, it's hard to be able to afford lowering prices. The same is true with adding selection. It's not hard to add lower ASP selection, it's hard to be able to afford offering lower ASP selection and still like the economics. Like improving speed, adding selection puts us in the consideration set for more purchases.”

One of the consequences of this investment and re-engineering is that per unit cost of a delivery has fallen for the first time in five years. The decline of $0.45 per package, when you are operating at the revenue scale and the relatively low margins that Amazon has, can make a huge difference.

“We can keep doing better on the cost to serve… the improvement in margins is not capped.” –

We can see the impact of these cost cuts on Shipping + fulfilment costs (S+F Cost) in the chart below.

Source: MBI Deep Dives

As the chart above shows, the S&F costs rose sharply during the pandemic but the rate of increase in costs has been brought down. The chart below shows the S&F Cost as a percentage of Gross Market Value (GMV).

Shipping+ fulfilment cost as a percentage of Gross Market Value (GMV) were 21.8% in 4Q 2023 (vs 26.1% in 1Q’22). Amazon believe there is more scope to cut this down further, perhaps closer to the 17% that prevailed in 2016.

Amazon GMV is about $800bn currently and therefore every 100bp improvement in the S&F cost/GMV percentage ratio, would add $8bn to Amazon’s annual net profit. A decline in the ratio from 21% to 17 % would increase net profit by $32 Bn. As a reference, the 2023 operating profit was $36bn.

Of course, these cost reductions are hard won, and very small numerical changes can take a long time to achieve. However, given current trends and management focus, it shows the kind of margin and profit expansion that could be achieved over the next 5 to 10 years.

“we're not done lowering our cost to serve. We've challenged every closely held belief for our fulfilment network and reevaluated every part of it and found several areas where we believe we can lower costs while also delivering faster for customers.”

AWS

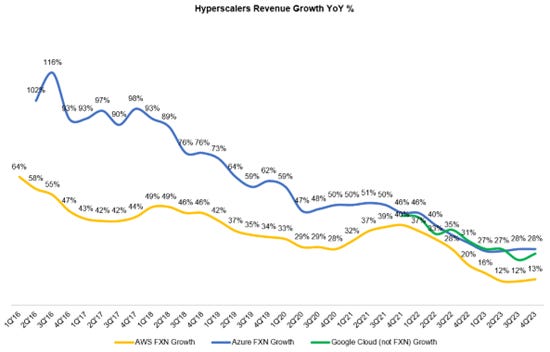

The demand for Cloud services increased during the quarter. AWS added $1.1 billion in revenue sequentially to $24 bn. AWS is an $100 bn annualized revenue business. We now have quarterly revenue data for cloud revenue growth for all three Cloud giants, Amazon, Microsoft and Google

Source: MBI Deep Dives

The latter two grew at 28% and 25% respectively, significantly higher than Amazon. As the largest player, Amazon continues to lose market share in the Cloud hosting space. In the next two years, Microsoft is likely to overtake AMZN and become the largest Cloud player.

Source: MBI Deep Dives

The Operating margin in AWS has recovered to 29.9%. These compare with 9% for Google and an estimated 40% for Microsoft (as they do not reveal the breakdown)

Generative AI:

As was the case for other large tech companies such as Microsoft, Alphabet and Meta Platforms, Generative AI was a big feature of the Amazon earnings conference call.

All the large tech companies are investing heavily in infrastructure and developing AI products and services. It is still very early stage in the AI Revolution, and nobody is sure how it will all develop in the long run.

Amazon outlined that their approach involves a three-layer tech stack.

“we've explained our vision of three distinct layers in the Gen AI stack, each of which is gigantic, and each of which we are deeply investing.”

The first layer involves algorithm training and inference. This where models are fed huge amounts of data and can learn patterns and structures. Amazon plans to use its internally developed chipsets and a partnership with Nvidia.

As we have noted before, AMZN has developed the Graviton chip, a CPU product for basic computing. The 4th generation of Graviton was released during the quarter, and it boasts 30% better performance than the predecessor.

Amazon also released the latest version of its Trainium chipset (so named based on its role to train models). It quadruples machine learning training speed vs the old model.

Amazon has also expanded its collaboration efforts with Nvidia to “deliver the most advanced infrastructure, services and software to power GenAI innovation.”

Amazon will be the public cloud player to deploy Nvidia’s latest Grace Hopper Superchips. The two are also working together to design the “world’s fastest” supercomputer to be hosted by AWS.

“At the bottom layer, where customers who are building their own models run training and inference on compute with a chip is the key component in that compute, we offer the most expansive collection of compute instances with NVIDIA chips.

We also have customers who would like us to push the price performance envelope on AI chips, just as we have with Graviton for generalized CPU chips, which are 40% more price performance than other X86 alternatives. And as a result, we built custom AI training chips, named Trainium, and inference chips, name Inferentia, and reinvent we now as Trainium2, which offers four times faster training performance and three times more memory capacity versus the first generation of Trainium, enabling advantageous price performance versus alternatives.

We already have several customers using our AI chips including Anthropic, Airbnb, Hugging Face, Qualtrics, Ricoh and Snap.”

The second layer is Model creation as a service. Amazon’s foundational Bedrock model on AWS is vital here. Bedrock allows developers working for AWS’s clients to build custom use cases on top of it, while also offering a plethora of 3rd party models such as Meta Platform’s Llama 2. As we observed in our recent note on Meta Platforms, Meta has taken an open platform approach where clients will get access to its Llama LLM model.

Gen AI is in a rapid experimentation phase at the moment. it is new field, and developers are actively moving between with different models to see which work the best for what they need.

Bedrock’s large partner integration roster allows these developers to freely move between model templates in a safe, secure, fully managed cloud environment.

During the quarter, AWS and Salesforce expanded their collaboration to add support for Bedrock in Salesforce’s ecosystem. Salesforce is also adding more AWS products.

AMZN claims Bedrock has “thousands of customers” and is “deeply resonating” with customers.

They argue clients want:

their Gen AI in the same cloud environment they’re learned and have grown to trust over years and years.

the cloud provider with the “best security track record.”

“In the middle layer where companies seek to leverage an existing large language model, customize it with their own data, and leverage AWS’ security other features all as a managed service, we've launched Bedrock which is off to a very strong start with many 1,000s of customers using the service after just a few months.

Security is a big deal, an important differentiator between cloud providers. The data in these models is some of the company's most sensitive and critical assets. With AWS' advantaged security capabilities and track record relative to other providers, we continue to see momentum around customers wanting to do their long-term Gen AI work with AWS. We're building dozens of Gen AI apps across Amazon's businesses, several of which have launched and others of which are in development.”

The third layer is the consumer app layer.

Amazon has introduced “Rufus” as a Marketplace shopping companion. This allows shoppers on its website to ask questions like “which football has the best grip” with detailed explanations taking you to the best option.

It’s trained on Amazon’s huge 40% share of U.S. ecommerce and commanding global commerce share, which competitors cannot match.

“This morning, we launched Rufus, an expert shopping assistant trained on our product and customer data that represents a significant customer experience improvement for Discovery. Rufus lets customers ask shopping journey questions like what the best golf ball is to use for better spin control …and get thoughtful explanations for what matters and recommendations on products.

Rufus is an expert shopping assistant trained on Amazon’s product catalogue and information from across the web to answer customer questions on shopping needs, products, and comparisons, make recommendations based on this context, and facilitate product discovery in the same Amazon shopping experience customers use regularly.”

They also emphasised the Amazon has been using AI for decades to develop products and services, currently being used, by millions of their customers.

“Amazon has been using AI very expansively for 25+ years to improve customer experiences. The personalized recommendations customers get when they shop Amazon’s store, the pick paths in our fulfilment centres, our drone deliveries, the conversational capabilities of Alexa, and our checkout-free Amazon Go stores are just a few examples of experiences fuelled by AI. And we believe generative AI is going to change virtually all customer experiences that we know.

Gen AI is and will continue to be an area of pervasive focus and investment across Amazon, primarily because there are a few initiatives, if any, that give us the chance to reinvent so many of our customer experiences and processes, and we believe it will ultimately drive tens of billions of dollars of revenue for Amazon over the next several years.”

Advertising

Advertising is a relatively new but fast-growing business for AMZN. In the breakdown given by the company, “Advertising and others” had $16bn revenues in Q4 2023. Given the scale of their business, with two million merchants of varying different sizes selling on their site, there is huge scope for sponsored advertisements.

“The strength in advertising was primarily driven by sponsored products as our teams worked hard to increase the relevancy of the ads, we show customers by leveraging machine learning. Advertising only works if the ads are helpful to customers and there's a lot of value in tailoring sponsored products, so they are relevant to what a customer is actually searching for. We're also continually focused on improving our measurement capabilities, which allow brands to see the payback of their advertising spend.”

AMZN is going to add advertising in Prime Video throughout 2024.

“Our advertising growth remains strong, up 26% year-over-year, which is primarily driven by our sponsored ads. We've recently added Sponsored TV to this offering in the U.S. a self-service solution for brands to create streaming TV campaigns with no minimum spend, putting this advertising within reach of any business. While still early days, streaming TV advertising continues to grow quickly. Brands are using our capabilities to reach engage viewers on Twitch, Freevee, Fire TV and Prime Video shows and movies, which just launched in the U.S., as well as Thursday Night Football.”

Conclusions

The quarter has been a very good one for Amazon.

They generated low double digit revenue growth, much higher margins.

They got the benefit of lower costs for shipping and fulfilment on a significantly expanded network,

The company believes it has further scope to reduce costs and given low margins, small changes in margins can have a significant impact on AMZN’s bottom line.

The likely change in business mix where the high margin business will grow faster will drive improvements in margins and profitability over the short to medium term

As is always the case, the AMZN stock looks optically expensive. However, the company has enough positive features and catalysts for us to continue to hold our small position in the stock.