Amazon.com (AMZN)

Q2 2025 Results

We have several written two notes on Amazon.com (AMZN). The first was an “Initiating Coverage” type note on 12 May 2023 and can be found here. In our biased view, it is definitely worth reading! The second was written after the Q2 2023 results and it can be found here. The most recent note can be found here.

We revisit the company again in the light of the recent Q2 2025 results.

Q2 2025

The headline was Amazon reported second-quarter results that beat the high end of guidance on both the top and bottom lines.

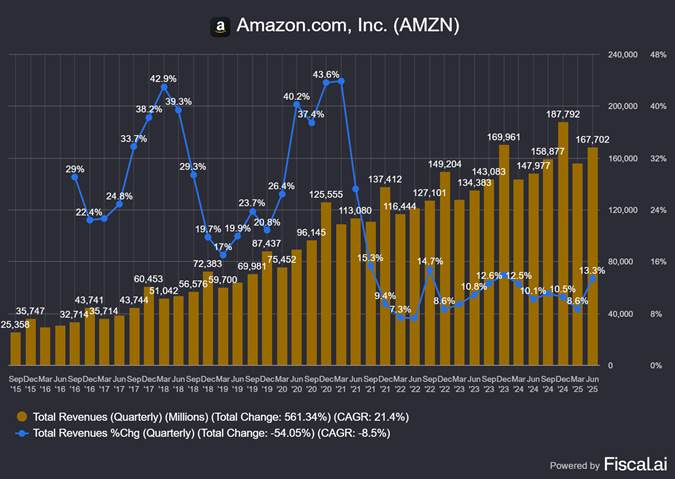

Total revenue was $167.7bn, a 13.3% increase (y/y) or 12% on a currency adjusted basis

Total operating income was $19.2bn which was up 30.7% (y/y)

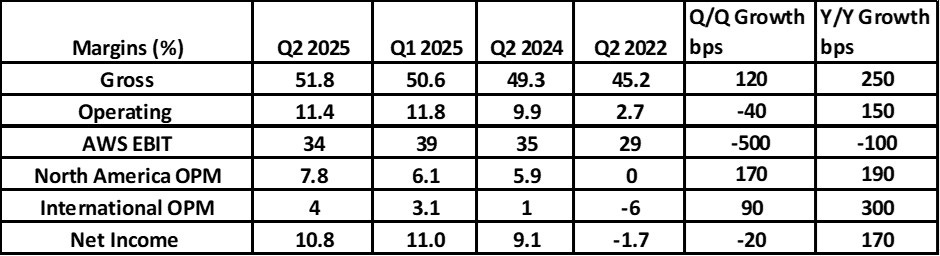

Operating Margin was 11.4% compared with 9.9% a year ago.

This suggests the company has considerable operating leverage.

Advertising revenue again grew strongly at an impressive 23% (y/y) and now accounts for 9% of total revenue.

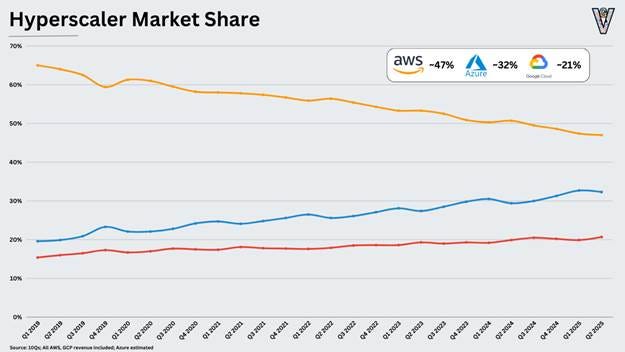

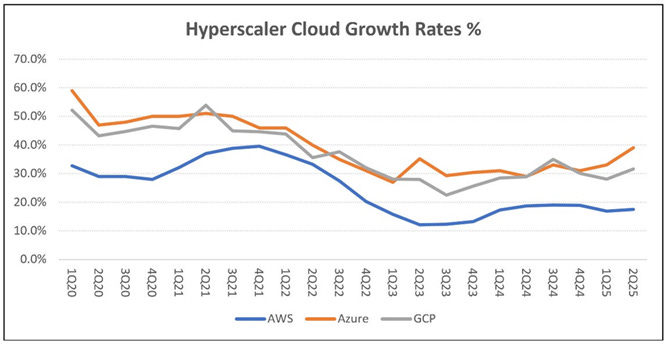

AWS revenue growth at 16.2% (y/y) was more than expected. However, it was much lower than the 39% and 32% recorded by the equivalent businesses at Microsoft and Google respectively.

AWS and the International segment saw above average revenue growth. North America revenue growth at 11.1% (y/y) was below average but North America continues to be dominant, accounting for 60% of the revenue.

Margins generally rose. The exception was AWS where margins fell 100bp (y/y) and are at their lowest level since Q4 2023 (see chart below) .

This was a good set of results but the markets responded negatively to the AWS numbers. Although AWS revenues were above guidance, growth was much less compared to their major competitors. AWS generated revenue of $30.9bn, up 16.1% (y/y). Microsoft Azure generated roughly $21bn in revenue, up 39% Y/Y. Google Cloud generated $13.6bn in revenue, up 32% Y/Y.

AWS has much higher operating margins than all other segments (except perhaps Advertising) and these have been on a rising trend for a decade. (See chart below).

The market was surprised by the decline in AWS operating margins in Q2 2025. A slowdown in sales and a decline in margins in the most profitable business segment was a source of significant concern.

Background

The trend in Amazon’s fundamentals had been of rising margins over the last decade. Both gross and operating profit margins have risen over the last decade. This reflects a consistent change in the business mix.

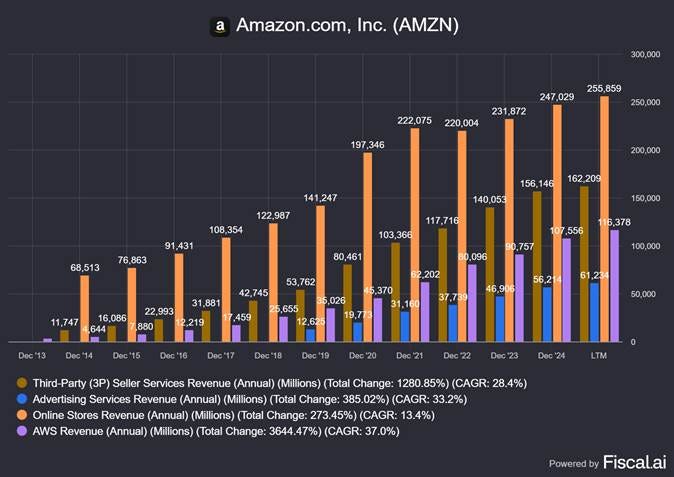

In a scenario of strong overall growth, the share of revenue accounted by first party online sales has consistently fallen in the last decade from about 75% in December 2014 to about 37% currently.

Higher margin business segments such as AWS, third party sales, subscriptions and, more recently, advertising have grown faster than average. Due to this change, average margins have has risen significantly.

There has also been rise in profitability. The chart below shows an increase in profitability as measured by Return on Equity (ROE) and Return on Invested Capital (ROIC).

The fundamentals of the business have improved thanks to the change in business mix.

AWS Growth

AWS grew more than expected in Q2 2025 but AWS margins decline. The company explained it as follows.

Revenue was $30.9bn, an increase of 17.5% (y/y) or 16.2% (y/y) on a currency adjusted basis. AWS now has an annualized revenue run rate of more than $123bn. During the second quarter, we continued to see growth in both our generative AI and non- generative AI businesses as companies turn their attention to newer initiatives bring more workloads to the cloud, restart or accelerate existing migrations from on-premise to the cloud and tap into the power of generative AI.

AWS’s operating margins fell due to stock-based compensation and an increase in depreciation.

AWS operating income was $10.2 billion and operating margins were 33% and declined sharply from 38% (q/q). About half is due to the seasonal step-up in stock-based compensation expense, driven by the timing of our annual compensation cycle. AWS margins also saw headwinds from higher depreciation expense .

AWS growth of 16.2% was much less than equivalent businesses at the next two large cloud hyperscalers, Microsoft Azure and Goggle Cloud Platform (GCP). The latter two grew quarterly revenue at 39% (y/y) and 29% (y/y) respectively.

Andy Jassy, the CEO of Amazon was asked why AWS grew more slowly than its main rivals.

He outlined a number of things including the fact that AWS is a much larger business

We have a meaningfully larger business in the AWS segment than others. I think the second player is about 65% of the size of AWS. it's still a pretty significant segment market segment leadership position that we have.

The rest of his answer was not very convincing.

The reality of what really matters is what customers' experiences are in operating on these platforms. And if you look at what matters to customers, what they care a lot about what the operational performances what the availability is, what the durability is, what the latency and throughput is of the various services. And I think we have a pretty significant advantage in that area.

Microsoft have had a number of security issues on their platforms and the Amazon CEO argued that this gave AWS an advantage.

And for most companies, they're putting data that they really care about in the cloud. The security and the privacy of that data matters a lot, and there are very different results in security in AWS than you'll see in other players. And yes, you could just look at what's happened in the last couple of months, you can just see kind of adventures at some of these players almost every month.

And so a very big difference, I think, in security. And then I think a really significant difference in functionality where not just in the core infrastructure, do we have a lot more functionality in our services. But I think if you look at our end-to-end offering in AWS in AI from the bottom of the stack all the way to the top, it's pretty different. So I feel good about the inputs and the services that we're offering to customers across AI as well as non AI and we have more demand than we have capacity right now.

They stated they are a large business and would like too grow more. At the very least this was an incomplete response.

So we could be doing more revenue and helping customers more, and we're working very hard on changing that outcome and how much capacity we have, but it's still like if you look at the business, it's $123bn billion annual revenue run rate business and it's still early. I

The answer in part probably does lie with the greater scale and size of AWS but it is by no means the whole story.

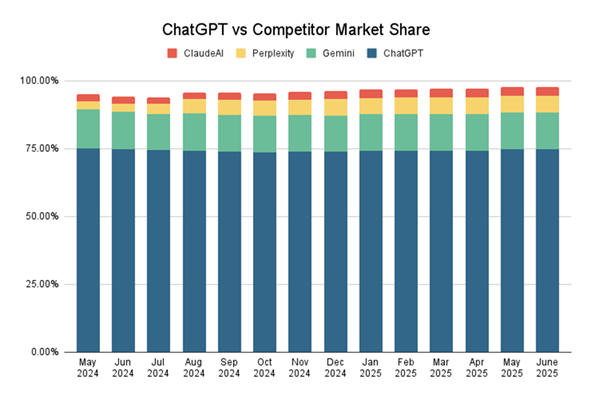

There is explosion of cloud infrastructure demand from the Gen AI players. The biggest and most successful player in this space is ChatGPT from OpenAI. It is far ahead of Google’s Gemini. Anthropic’s Claude, Perplexity and others.

ChatGPT commands an estimated 75% AI market share. Their business scale is growing rapidly and so is their need for cloud infrastructure.

Microsoft has a right of first refusal to supply new capacity to OpenAI. Open AI’s huge need for compute and infrastructure is a great boost to Microsoft’s Azure business. This shows yet again how attractive the deal between Microsoft and Open AI is for the former.

Microsoft’s relationship with OpenAI began in 2019 with an investment of just $1bn. In total, it has invested $13.75bn in return for a 20% share of revenues and profits up to a total of $ 92bn. If this is achieved Microsoft would see a return of at least 6.7X.

Microsoft Azure provides cloud hosting for OpenAI’s rapidly growing business, which is currently at about $1bn of annual revenue, for Microsoft and likely to grow fast. This is subject to a 20% revenue rebate. Given likely margins, this is a highly profitable revenue stream for Microsoft, even after accounting for the rebate.

The agreement favours Microsoft. It may have been reasonable for OpenAI six years ago, but it now looks a poor deal given the exponential growth in OpenAI revenues and profits since then.

OpenAI wants to renegotiate the agreement and look for a path to convert to a regular for-profit company. Microsoft is playing hardball. The negotiations have been reported as being difficult.

OpenAI has recently entered partnerships with Goggle, CoreWeave and Oracle via the StarGate project to expand infrastructure requirements.

Google Cloud Platform (GCP) also benefits from hosting Google AI offerings such as the Gemini family of models, NotebookLM, Veo3 etc etc.

Amazon’s Nova LLM has not gained much traction. Amazon has a stake in Anthropic but the latter’s Claude is also available on GCP as well as AWS.

The dominance of ChatGPT helps Azure’s numbers and makes AWS look less good in comparison. Amazon CEO acknowledged this in the Q&A but argues it is early in the AI game and AWS will see growing demand in the future from new products such as millions of AI Agents.

You have a small number of very large frontier models being trained that spend a lot on computing, a couple of which are being trained on top of AWS and others are being trained elsewhere.

And you also have a relatively small number of very large-scale generative AI applications. The one category would be chatbots with the largest by a fair bit being ChatGPT.

Amazon claims there are many AI companies which are on AWS but they are in pilot mode so their revenue contribution is not yet large.

The other category being, coding agents. So these are companies like Cursor, Vercel, Lovable and some of the companies like that. They run significant chunks on top of AWS. And then you've got a very large number of generative AI applications that are in pilot mode -- or they're in pilots or that are being developed as we speak and a very substantial number of agents that also people are starting to try to build and figure out how to get into production in a broad way, but they're all -- they're quite early.

We have a very significant number of enterprises and startups who are running applications on top of AWS' AI services . It's still just earlier stage than it's going to be

All large players have said they are capacity constrained, they cannot supply existing demand and they continue to make additional investments .

AWS backlog was $195bn and that is up about 25% (y/y). We have more demand than we have capacity at this point. And I think that -- and you see some of the constraints and they kind of exist in multiple places, the single biggest constraint is power.

I don't believe that we will have fully resolved the amount of capacity we need for the amount of demand that we have in a couple of quarters. I think it will take several quarters. But I do expect that it's going to get better each quarter, and I'm optimistic about that.

The impact of tariffs.

Given the size of their retail business, US tariffs on imports will have a big impact,

There continues to be a lot of noise about the impact that tariffs will have on retail prices and consumption. Much of it thus far has been wrong and misreported. As we said before, it's impossible to know what will happen.

If costs end up being higher, who will absorb them, but what we can share is what we've seen thus far, which is that through the first half of the year, we haven't yet seen diminishing demand nor is price meaningfully appreciating.

They have over 2 million (!) third party sellers. Each one will decide whether to pass on the cost of the tariffs or whether to absorb some of it.

We also have such diversity of sellers in our marketplace over 2 million sellers in total with different strategies of whether to pass on higher cost to consumers, the customers are advantaged shopping at Amazon because they're more likely to find lower prices on the items they care about.

Improving delivery speeds by investing in logistics

Amazon outlined the incremental progress they continue to make in increasing the speed of deliveries and in reducing costs.

Further improving delivery speed remains a key focus, and we continue to make progress. We've previously shared how we re-architected our U.S. inbound network into a regional structure, allowing us to place inventory and ship from locations closer to customers, improving speed and low run costs.

That work is delivering tangible results. In Q2, we increased the share of orders moving through direct lanes( where packages go straight from fulfillment to delivery without extra stops) by over 40% (y/y).

We've also reduced the average distance packages traveled by 12% and lowered handling touches per unit by nearly 15%. We've made progress on order consolidation with more products positioned locally, we're able to pack more items into each box and send fewer packages per order.

Taken together, these improvements are making the network faster and structurally more efficient.

We've also set another global speed record in Q2 delivering to prime members at our fastest speeds ever. In the U.S., we delivered 30% more items same day or next day than during the same period of last year.

We've recently announced plans to expand our same-day and next-day delivery to tens of millions of U.S. customers and more than 4,000 smaller cities, towns and rural communities by the end of the year. Today, it's already available in more than 1,000 of these communities across the U.S.

The early response from customers in these areas have been very positive.

We deployed our 1 millionth robot across our global fulfillment network and unveiled innovations in our last-mile innovation center, such as automated package sorting and a transformative technology that brings packages directly to employees in an ergonomic height.

Amazon Advertising

Advertising is the fastest growing business withing Amazon. We have not seen data on the segment’s operating margins but they are likely to be high.

We're pleased with the strong growth, generating $15.7bn of revenue in the quarter, growing 22% (y/y) .

We continue to see strength across our broad portfolio of full funnel advertising offerings that in the U.S. alone help advertisers reach an average ad-supported audience of more than 300 million across our own properties.

They continue to develop their own Demand Side Platform (DSP) which help advertisers run targeted campaigns. This will help them target audience both within and outside the Amazon ecosystem.

Another area we're excited about is our demand side platform, or Amazon DSP. Our DSP enables advertisers to plan, activate and measure full funnel investments.

Our trillions of proprietary browsing, shopping and streaming signals paired with extensive supply side relationships and our secure clean rooms provide advertisers the ability to optimize advertising, deliver greater precision and drive efficient and effective advertising outcomes.

In June, we announced a momentous partnership with Roku, giving advertisers access to 80mn connected TV households. The largest authenticated connected TV footprint in the U.S. exclusively through Amazon DSP is a giant leap forward for advertisers bringing best-in-class planning, audience precision and performance to TV advertising.

We also announced an integration between Disney's real-time ad exchange and Amazon DSP. This collaboration allows advertisers to gain direct access to Disney's premium inventory across platforms like Disney+, ESPN and Hulu while allowing them to leverage insights from both companies.

International.

Operating margins in the international segment are at 4%: half the 8% prevailing in the US market. However, both have been improving over time.

AMZN management gave a breakdown of the international business which has two segments; established countries and emerging countries.

One is the the established countries like U.K., Germany and Japan, already at similar margin profiles to the U.S. -- as they continue to grow their contribution of profit will grow over time,

In our emerging countries, we're pleased with the progress we're making there. We've launched 8 countries, of course, in the last 5 years. And there are all varying degrees of upfront investment in different point in times in their journey to profitability, but they're all making very nice improvements quarter- over-quarter in growing selection, adding prime members and expanding our customer offerings.

Summary.

This was a good set of quarterly results for Amazon. The giant machine founded by Jeff Bezos continues to grind on remorselessly.

The company achieved double digit growth in revenue and earnings growth and demonstrated significant operating leverage

Markets were concerned by AWS , the cloud hosting business. AWS revenue growth at 16.2% was less than similar business units at Microsoft and Google. AWS operating margins fell by 100 bps.

As noted above, the explosive growth in AI LLM -driven demand has favoured Microsoft and Google more than Amazon. The latter continues to have significant strengths and the whole industry faces a huge demand/supply imbalance which will only be resolved in the medium term.

AWS margins declined in part due to higher depreciation charges. This will be an issue for all hyperscalers as they have all boosted Capital Expenditure in recent years.

The decade-long trend at Amazon is of improving margins and profitability thanks to change in business mix.

Over the same period valuations as measured by P/E Ratio and P/S ratios have been stable.

This combination of improving fundamentals and steady valuations means the investment case for Amazon is improving over time.

Valuation and Conclusions.

At the current share price of $221 per share, the stock is trading at a two-year forward P/E ratio of 29.2X, and a three year forward PE ratio of 24X which is either fair value or a little expensive for a company with an ROE of 24% and a likely earnings growth of 13% to 16% on the next two to three years.

We have a nominal 1.5% holding in AMZN. We have preferred MSFT, NVDA and others as better AI/Cloud plays.

We will hold onto our Amazon position, We will keep a close eye on it as the valuation is very gradually getting more attractive.